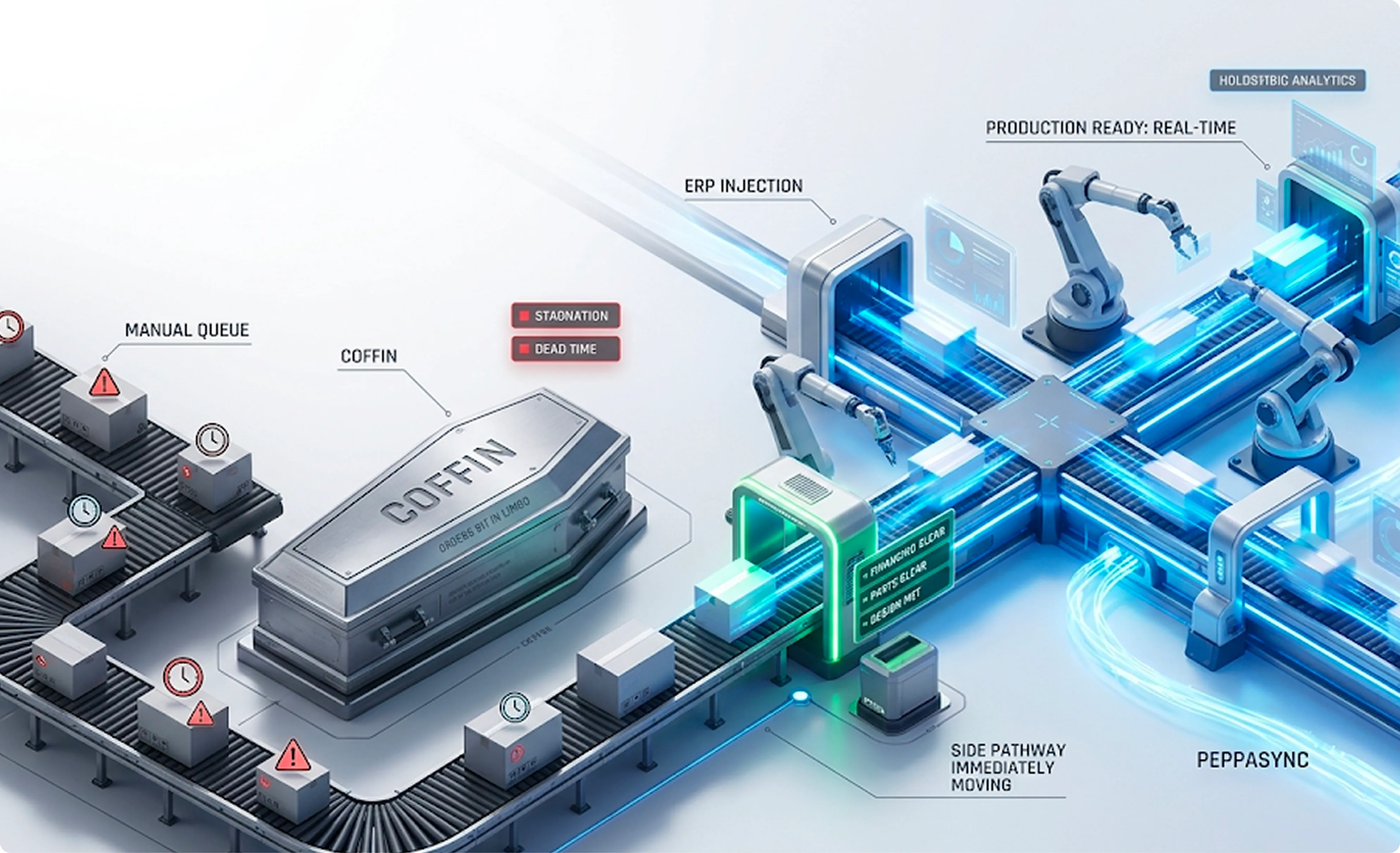

A high-value order arrives at a factory that builds things to spec. The customer paid a deposit, the financing is conditionally approved, two of the four required materials are in the warehouse. The order sits in a spreadsheet maintained by someone in operations who audits the file twice a week. By the time the operations person notices that all four conditions have cleared, 48 hours have passed and a production slot that could have been filled is sitting empty. The factory loses the margin on a $50,000 build because the data lived in the wrong place for two days.

Peppasync, the product Banky Alao is now building, exists because of this specific problem. It is software that watches the conditions around a complex order, financing, materials, customer specifications, and pushes the order to the factory ERP the moment everything has cleared. The wait becomes automated. The data coffin disappears.

What is interesting is not the product. What is interesting is what it used to be.

The pivot

In 2022, Banky Alao took Peppa through Techstars. The product then was a purchase-protection app for social commerce in emerging markets. The problem it addressed was scam culture on social platforms: $770 million in 2021 alone lost to fake sellers who pocketed pre-payments and disappeared. Peppa held the buyer’s money in escrow until delivery, distributed through embedded integrations with banks and mobile wallets. By the end of the first 5 months it had acquired 1,000 merchants, 25 percent GMV growth, and partnerships with Tier 1 banks including First Bank.

3 years later, that product is gone. The website that now lives at peppasync.ai describes something almost unrecognizable: an enterprise B2B platform for connecting Shopify to Microsoft Dynamics 365 in build-to-order commerce. Different customer (factory operators, not social-media buyers). Different problem (orchestration lag, not fraud). Different price point ($50k orders, not $50 transactions). Different geography (the headline customers are global retailers, not emerging markets). Different sales motion (enterprise contracts, not embedded consumer apps).

The team remains. Banky in Birmingham. His co-founder and CTO Emmanuel Obute in Lagos. 9 employees, down from 14 at the Techstars peak. The company kept the name and threw out the product.

The bet

The interesting question is whether the pivot is as discontinuous as it looks. Read the surface and it’s two different startups in two different markets. Read closer and there’s a thread.

Both products are infrastructure for transactions that need multiple systems to coordinate before they can complete. The anti-scam app held money in a clean limbo until both buyer and seller had done their parts. Peppasync holds an order in a clean limbo until financing and materials have done theirs. Banky’s word for what Peppasync does is “persistence layer,” and that’s exactly what the original product did too. The customer changed. The infrastructure problem rhymes.

The bet underneath this version is that mid-market and enterprise BTO commerce has been waiting for someone to build proper orchestration software, and that the legacy ERP systems are too rigid to do it themselves. ERPs are built to process clean records, not to wait on partial ones. Spreadsheets are what fills the gap, and spreadsheets introduce 48-hour delays where a clean integration would close in seconds. If Peppasync can convince a few enterprise customers that the infrastructure is worth paying for, the rest of the BTO sector tends to follow the early adopters.

The harder question is whether a 9-person team with a B2C consumer fintech track record is the team to sell enterprise B2B factory software. The buying motion, the customer profile, the sales cycle, the deal sizes, the implementation requirements, none of it overlaps with what Peppa learned at Techstars. The team is rebuilding their go-to-market muscle in public.

What to watch

The category Peppasync is now competing in includes Workato, Tray.io, Boomi, and Microsoft’s own Power Automate. Established players with distribution and enterprise references. Peppasync is differentiating on a vertical (build-to-order commerce specifically) rather than on breadth, which is the right move for a small team but also a narrower addressable market than the generic integration platforms.

2 things will tell us whether the bet is working. Whether the V1 Early Access cohort produces a few named enterprise design partners who publicly endorse the product, since enterprise software lives or dies by named references. And whether Banky and Emmanuel can pull more operations and enterprise-sales DNA into the team in the next 6 months, since the founding crew is engineering- and consumer-product-heavy and the new motion requires people who can sell to operations directors and CFOs.

What we’re rooting for

We’re rooting for Peppasync to add 25 new enterprise design partners during the V1 Early Access program by end of Q3. That’s a stretch for a small team selling into enterprise but a real signal that the pivot is finding its market. Spotlight is cheering every signed partner, and we hope Banky comes back to share the win when the V1 cohort lands.

Enterprise teams interested in joining the V1 Early Access program can contact the business team.